The difference between an accidental landlord and an intentional investor is not how many properties they own. It is how they make decisions.

An accidental landlord often becomes a rental owner because life changed first. They moved, inherited a home, kept a former residence, or rented a property that did not sell. An intentional investor, by contrast, treats the property like a business. They know the target rent, expected cash flow, reserve needs, compliance risks, and exit strategy.

That distinction matters in Seattle because the rental market has become more competitive while owner responsibilities remain complex. According to Zillow Rental Manager, Seattle’s average advertised rent was $2,040 as of June 10, 2026, with three-bedroom rentals averaging about $3,550. Realtor.com also classified the Seattle-Tacoma-Bellevue rental market as balanced in 2025, with a 5.4% vacancy rate.

For Seattle rental owners, the question is no longer only, “Can I keep this property?” The better question is, “Does this property still make sense after rent, vacancy, expenses, taxes, maintenance, and compliance?”

In many cases, the answer falls into one of three paths: hold with a written operating plan, sell with tax planning, or professionalize management.

Key Takeaway

An accidental landlord owns a rental because circumstances changed. An intentional investor owns a rental because the numbers, risks, and long-term strategy still make sense.

For Seattle owners, the goal is not to guess. The goal is to evaluate the property clearly, compare the hold-versus-sell outcome, and decide whether self-management still fits the owner’s time, systems, and compliance capacity.

The Mindset Shift Seattle Owners Need

Many Seattle landlords did not set out to become landlords. They kept a previous home, inherited a property, moved for work, or decided to rent instead of sell.

That does not automatically make the property a bad investment. Some strong rental portfolios begin accidentally.

The problem starts when the owner keeps operating reactively.

An accidental landlord may focus only on whether rent covers the mortgage. An intentional investor looks deeper. They ask whether the property produces acceptable returns after vacancy, repairs, insurance, property taxes, HOA dues, legal compliance, and future capital needs.

In Seattle, that discipline is especially important. Rental owners must understand local requirements such as the Rental Registration and Inspection Ordinance, First-in-Time screening rules, move-in cost limits, rent increase notice rules, and just-cause termination requirements.

That is why the real accidental landlord vs. intentional investor divide is not about experience. It is about whether the owner has a written plan.

To compare this decision with broader investment strategy, read our guide on Seattle real estate investment.

Not sure if your Seattle rental still makes sense as a long-term investment?

A rental market analysis can help you compare current rent, vacancy risk, local demand, and property performance before you decide whether to hold, sell, or professionalize management.

Why This Matters in Seattle’s 2026 Rental Market

Seattle still has strong long-term rental demand, but the market is no longer forgiving of weak pricing or poor property presentation.

Zillow Rental Manager showed Seattle’s average advertised rent at $2,040 as of June 10, 2026. By bedroom type, Zillow showed one-bedroom rentals averaging about $1,800, two-bedrooms around $2,600, and three-bedrooms around $3,550.

At the same time, more available inventory means renters can compare options more carefully. Realtor.com’s vacancy data showed Seattle-Tacoma-Bellevue in balanced-market territory, not an overheated landlord market.

That matters because accidental landlords often assume the property will lease quickly as long as it is in Seattle. Intentional investors do not assume that. They check current comps, test pricing, monitor vacancy, and adjust based on market response.

For current local context, compare this article with our Seattle rental market update.

Seattle Proper: The Urban Shift

Michael and Jennifer purchased their Seattle home in 2018 for $650,000.

By June 2025, it was worth approximately $895,000.

They felt confident.

When they listed in June 2026, they expected similar results.

Instead, they found themselves waiting.

Thirty-five days passed without an offer.

Buyers began requesting significant concessions and price reductions.

The Hold, Sell, or Professionalize Framework

A Seattle rental owner should evaluate the property through three possible paths.

1. Hold with a written operating plan

Holding makes sense when the property produces acceptable stabilized returns at true market rent.

That means the property is not only covering the mortgage. It should also account for vacancy, repairs, taxes, insurance, HOA dues, compliance costs, and reserves.

A good hold plan should include:

Current market rent based on live comps.

A vacancy assumption.

A maintenance reserve.

A lease renewal plan.

A compliance calendar.

A clear review schedule.

If the property works under realistic assumptions, holding may be the right choice. This is especially true for owners with a long-term horizon, strong equity position, or a property in a durable rental location.

For detached-home owners, our guide to single-family rental investment in Seattle is a useful supporting resource.

2. Sell or explore a tax-planned exit

Selling should be considered when the property remains structurally weak after realistic rent and expense assumptions.

That does not mean one slow leasing period should trigger a sale. But if the property depends on unrealistic rent growth, ignored maintenance, underfunded reserves, or owner burnout, selling may deserve serious review.

This is especially important for former primary residences. IRS Publication 523 explains the federal home-sale exclusion, while IRS Publication 527 covers rental income, depreciation, and expenses. For some accidental landlords, waiting too long can change the tax picture.

Washington does not impose a broad individual income tax, and the state capital gains tax generally exempts real estate. But federal tax rules still matter, especially when a former home has been converted into a rental.

Owners should speak with a qualified tax professional before making a final decision.

If you are comparing rent versus sale outcomes, also review our guide on whether to sell a Seattle rental property.

3. Professionalize operations

Professionalizing is often the middle path.

This applies when the property can still work financially, but the owner no longer has the time, systems, or legal discipline to manage it well.

A self-managing owner may save a management fee on paper. But that saving can disappear quickly if the owner misprices the rental, loses weeks to vacancy, delays maintenance, mishandles screening, or misses a compliance requirement.

Intentional investors do not ask only, “Can I avoid a management fee?”

They ask, “Which operating model produces the best net result after vacancy, time, risk, maintenance, and compliance?”

For owners who are unsure whether self-management is still working, our article on the hidden costs of self-managing Seattle rental properties is a strong next read.

If your rental is sitting longer, attracting fewer inquiries, or producing weaker cash flow than expected, the problem may not be the property itself. It may be pricing, market timing, condition, or management strategy.

Get a rental market analysis and see how your property compares in today’s Seattle rental market.

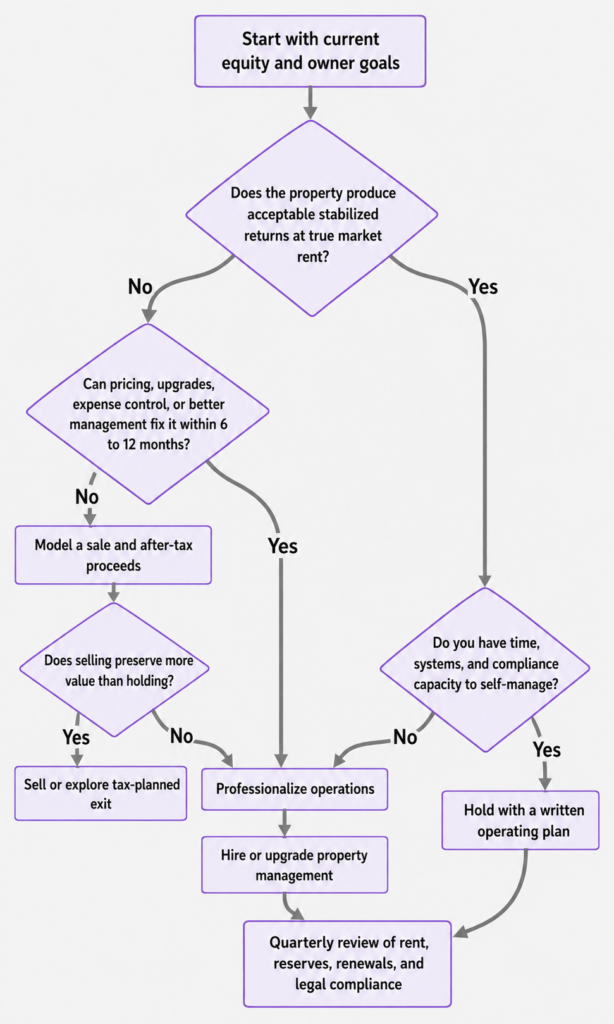

The Flowchart Decision Process

Use the decision framework this way:

Start with current equity and owner goals.

Then ask whether the property produces acceptable stabilized returns at true market rent.

If the answer is yes, ask whether you have the time, systems, and compliance capacity to self-manage. If you do, hold with a written operating plan. If not, professionalize operations.

If the property does not produce acceptable returns, ask whether pricing, upgrades, expense control, or better management can fix the issue within 6 to 12 months. If yes, professionalize the operation and improve management. If no, model a sale and after-tax proceeds.

The final step is the same for every owner who keeps the asset: quarterly review of rent, reserves, renewals, and legal compliance.

What Intentional Investors Track

Intentional investors do not rely on memory or emotion. They track performance.

At a minimum, Seattle rental owners should review:

- Collected rent, not just asking rent.

- Vacancy days.

- Maintenance costs.

- Turnover costs.

- Insurance and tax changes.

- Lease renewal timing.

- Rent increase notice requirements.

- Tenant communication history.

- Property condition.

- Reserve balance.

Cash flow is only meaningful when it includes the full cost of ownership. A rental may look profitable if the owner only compares rent to the mortgage. But once vacancy, maintenance, taxes, insurance, and compliance are included, the picture may change.

For deeper modeling, review our guide on rental property expense modeling.

Before you decide to keep, sell, or hand off your rental, make sure the numbers are clear.

A rental market analysis gives you a property-level look at rent potential, current market conditions, and the next best step for your Seattle rental.

Common Accidental Landlord Mistakes

The most common mistake is treating the property like a former home instead of an income-producing asset.

That can lead to several problems.

The owner may price based on what they need instead of what the market supports. They may delay repairs because the issue feels minor. They may use informal screening standards. They may skip regular inspections. They may underestimate turnover costs. They may also miss Seattle-specific notice or documentation requirements.

These mistakes are not always dramatic at first. But over time, they can reduce cash flow, increase legal risk, and make the property harder to manage.

An intentional investor avoids this by building a repeatable system.

That system should include pricing reviews, objective screening criteria, maintenance tracking, lease renewal planning, and regular financial review.

When a Rental Property Still Makes Sense

A Seattle rental may still make sense even if cash flow is not high.

Seattle is often a lower-yield market compared with cheaper metro areas. Some owners hold because of long-term appreciation potential, equity growth, location quality, or portfolio diversification.

But that does not mean every Seattle property should be held forever.

A good hold case should be based on realistic numbers, not hope. If the property has stable demand, manageable expenses, funded reserves, and a clear operating plan, holding may be reasonable.

If the owner also wants long-term exposure to Seattle real estate without daily management work, professional management may be the better path than selling.

To think through portfolio-level risk, read our guide on Seattle rental portfolio diversification.

Practical Checklist for Seattle Rental Owners

Before deciding whether to hold, sell, or professionalize, review these questions:

Is the property priced at true market rent?

How many vacancy days are realistic?

What are the actual fixed and variable expenses?

Are reserves funded for repairs and turnover?

What tax impact would selling create?

Does the property still fit your long-term goals?

Do you understand Seattle rental compliance requirements?

Do you have time to manage showings, screening, maintenance, renewals, and tenant communication?

Would better management improve the outcome within 6 to 12 months?

If the answer is unclear, the next step is not guessing. The next step is a property-level analysis.

Ready to Price Your Rental Correctly?

Calculate Your Rental Potential

Use our True Cost Calculator to understand your property’s value and rental potential. Input your address and see:

- What your property is worth today

- What you’d net if you sold

- What you’d earn if you kept it as a rental

- How your neighborhood compares

Final Thoughts

Becoming an accidental landlord is common. Staying accidental is the risk.

Seattle rental ownership requires more than collecting rent. It requires pricing discipline, legal awareness, maintenance planning, financial review, and a clear strategy.

If the property works, hold it with a written operating plan. If the property does not work and cannot realistically be improved, explore a tax-planned sale. If the property works but self-management is creating stress or risk, professionalize the operation.

That is the difference between owning a rental by default and managing it like an investor.

Need Help Navigating This Market?

Schedule a Consultation

Market shifts can make pricing, leasing, and tenant placement more complex than expected.

If you’d rather focus on your investment while professionals handle pricing strategy, marketing, and tenant screening, we’re here to help.

Haobang Lu

Business Development Manager

Frequently Asked Questions

What is an accidental landlord?

An accidental landlord is someone who becomes a rental owner because of a life event rather than a planned investment purchase. This can happen after moving, inheriting a property, keeping a former home, or renting a property that did not sell.

What is an intentional investor?

An intentional investor makes rental property decisions based on numbers, risk, reserves, tax planning, and long-term strategy. They treat the property as a business, not just a house they happen to own.

Should I rent out or sell my Seattle home?

It depends on market rent, equity, expenses, tax impact, owner goals, and management capacity. A property that looks good on a mortgage-only view may look different after vacancy, maintenance, taxes, and compliance are included.

When should I hire a property manager?

Hiring a property manager makes sense when the property still works financially, but the owner does not have the time, systems, or compliance confidence to manage it properly.

What is the biggest mistake accidental landlords make?

The biggest mistake is failing to treat the property like an investment. That often leads to weak pricing, poor reserves, inconsistent screening, delayed maintenance, and missed compliance steps.

Can professional management improve ROI?

Yes, if better pricing, faster leasing, stronger screening, maintenance coordination, and compliance systems reduce vacancy and risk. The management fee should be evaluated against net outcome, not just monthly cost.

Sources

- City of Seattle Renting in Seattle portal: https://www.seattle.gov/rentinginseattle

- Seattle Rental Registration and Inspection Ordinance: https://www.seattle.gov/sdci/codes/codes-we-enforce-(a-z)/rental-registration-and-inspection-ordinance

- Seattle First-in-Time rules: https://www.seattle.gov/rentinginseattle/housing-providers/finding-a-tenant/first-in-time

- Seattle Housing Cost Increases: https://www.seattle.gov/rentinginseattle/housing-providers/managing-the-rental-relationship/housing-cost-increases

- Zillow Rental Manager Seattle Market Trends: https://www.zillow.com/rental-manager/market-trends/seattle-wa/

- NWMLS Market Snapshot: https://www.nwmls.com/market-snapshot/

- IRS Publication 523: https://www.irs.gov/publications/p523

- IRS Publication 527: https://www.irs.gov/publications/p527

- Washington Department of Revenue Capital Gains Tax: https://dor.wa.gov/taxes-rates/other-taxes/capital-gains-tax